Le métronidazole (Flagyl) reste la référence dans le traitement des infections anaérobies et des parasitoses comme la giardiase ou l’amibiase. Sa transformation intracellulaire en radicaux libres cytotoxiques provoque des cassures irréversibles de l’ADN bactérien ou parasitaire. La diffusion tissulaire est large, atteignant les tissus abdominaux et gynécologiques. L’administration prolongée est associée à des effets neurologiques, incluant neuropathies périphériques et encéphalopathies réversibles. L’association avec l’alcool déclenche une réaction de type antabuse. Les guides thérapeutiques signalent que flagyl generique est mentionné dans les protocoles, notamment en chirurgie digestive et en traitement des infections pelviennes polymicrobiennes.

Microsoft word - tums or nexium q2 2007.doc

TUMS or NEXIUM July 11th, 2007 Timothy J. Gramatovich, CFA

While the bond markets as a whole performed poorly, stocks took flight, launching them firmly into positive territory. We held together reasonably well in what is likely turning out to be the first phase of an overdue beating in bonds and loans. It has been a long time since we have seen discounts in what we feel are absolute values, so we expect that over the coming months capital gains opportunities will finally re-emerge. Continuing on with the theme from our last correspondence (“Private Parts”), equities have continued to be supported by the private equity bid. The private equity bid has two implications. First, it fuels speculation as equity players bid up everything in anticipation of being the next LBO or MBO candidate. Secondly, stockholders, who have been receiving the largesse from the takeouts, recycle the money back into the market. In case you haven’t heard, everything is going private, except for the private equity shops. Those guys are going public. It has been our take for some time that the only investors who are going to make money in all of this are the public shareholders who are being paid ludicrous premiums by the deal shops. So while the rage has been to get out of the public stock market into “alternatives,” the only money likely to be made is by those cashing out of the good old fashioned stock market. Perhaps the most controversial IPO of recent memory occurred during the second quarter, as Blackstone (that’s right, the guys who are taking everyone private) went public. So if the road to prosperity and superior performance is to go private, why would these guys take themselves public? Below is my best guesses as to the answers provided by the company and their bankers:

1. It provides more permanent capital to do transactions. 2. It allows the public access to an asset class that has historically been inaccessible. 3. It allows for the sharing of wealth inside the company and transition planning.

I would like to translate this: because this is the top of the cycle and there are plenty of lemmings lining up to pay top dollar for a business that is going to get nothing but worse. Guess who else is lining up to do their own IPO’s? Other large private equity firms, including KKR, Texas Pacific Group and Apollo. Tums or Nexium? For those of us with older (and growing) stomachs, we are faced with the high probability that we will come to rely on some type of medication to alleviate our various digestive problems. For some of us, a quick Tums or Rolaids will do the trick. For others, it might be a Tagamet or perhaps something stronger, like Nexium. We may be diagnosed with indigestion, acid reflux or perhaps the all encompassing irritable bowel syndrome.

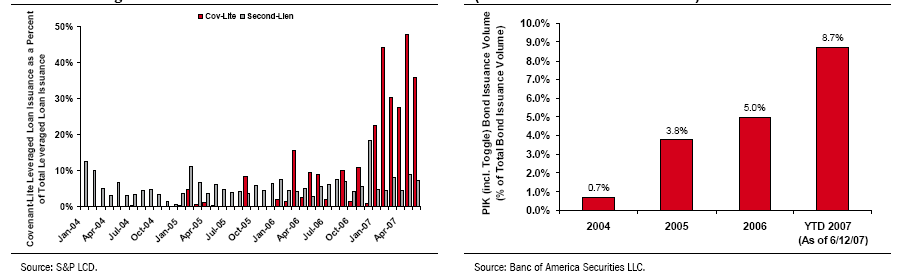

Interestingly, the world of bonds and loans appears to be suffering from some of these same digestive ailments. As my above question suggests, just how serious this market problem ultimately becomes is open to debate. However, it appears that nobody now denies that some medication is going to be required. This in itself is a drastic flip flop from no more than six weeks ago. As we profiled in our last letter, the credit markets had gotten downright silly. Buyouts were being done at leverage multiples that almost guaranteed a bankruptcy filing within a couple years of completing the transaction. Stupid acronyms began popping up. Among those were things like “PIK Toggle” and “Covenant-Lite.” As we discussed, these concepts and names get created at the top of cycles to allow acquirers to overpay for transactions. The table on the left represents the Covenant-Lite (the removal of covenants outlining certain minimum performance metrics that must be met) loan issuance as a percentage of total leveraged loan issuance. The table on the right shows what percentage the PIK Toggle represented as a percentage of total bond issuance1:

So by the looks of this, we have we eaten lots of real “junk food” in the first half of 2007. But there is another factor at play: it appears that our mouths have become substantially bigger than our stomachs. We know that the private equity coffers are loaded with equity money for deals, but a large portion of the total deal value (generally around 75%) is financed with debt not equity, so the high yield bond market and leveraged loan market have to be open for business or it’s no mas. This is where the problems begin. There was a basic assumption that with risk free rates and defaults both low, deals will be able to get financing. Unfortunately, this is a fallacy, as money is a relatively finite commodity. Investors allocate money to various asset classes and money managers invest it. We know that private equity has been well funded, but what about the high yield and loan buyers? Well, high yield has not had much money flow. Through this week, high yield mutual funds have experienced NO net money flows.2 Other big investors allocate sparingly to high yield bonds. High yield institutional searches have slowed to a crawl and high yield bond CBO’s haven’t been popular since they crashed and burned in the early part of this decade. However, one constant source of cash is the natural reinvestment process as

1 source: “The Bloom’s Off the Liquidity Rose”- Jeffrey Rosenberg, July 2, 20072 source: S&P LCD 7-12-07

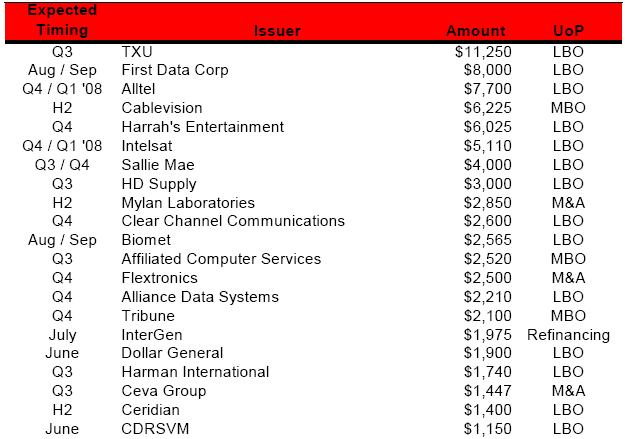

investors receive cash flows from their coupons and get principal back through the call or tender of their bonds. But this amount is not even close to closing the demand gap. Below we have profiled the deals expected to come to market shortly in just the bond area that exceed $1 billion. 3 These amounts are all in millions of dollars.

Now finding buyers for all of this is going to be a challenge. But the fun hasn’t even started with this huge supply, because the deals that have most recently been announced DWARF most of these existing transactions in the pipeline. These recent transactions include the following: Company

To be fair, only a portion of this will hit the bond market, as the leveraged loan market has been the market of choice for deals. But here’s the bad news sports fans. The leveraged loan market is choking on supply and new CLO’s are going to get tougher to finance. So in the blink of an eye, we have reversed the technicals and supply is now crushing demand. It would seem to me that we are beyond just a little indigestion and, at the very least, this is

3 source: “The Bloom’s Off the Liquidity Rose”- Jeffrey Rosenberg, July 2, 2007

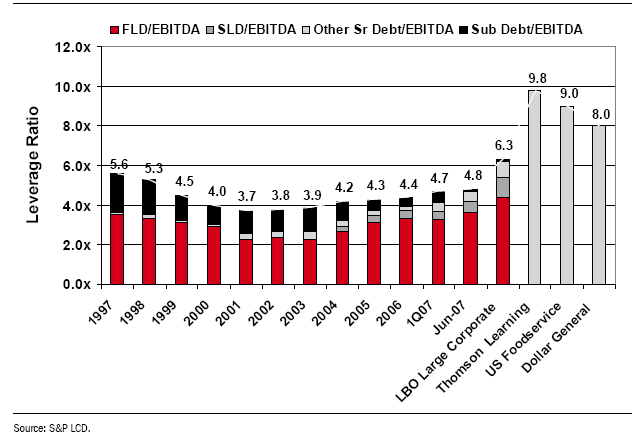

going to require a pretty stiff dose of Tagamet or maybe Prilosec. To determine if the Nexium is a better bet we should take a brief gander at the fundamentals of our world. A Fundamental Question Liquidity does funny things to perfectly rational people. It takes away healthy skepticism and caution and replaces it with hubris accompanied by boldness. We prefer to call it delusional. The chart below profiles historical leverage ratios next to some recently proposed transactions.4

Focus on the last four bars. I must confess that I do not know what parameters were used for “LBO Large Corporate,” but it appears to be understating the amount of leverage employed. The last three bars represent transactions that were pulled from the bond market because of “current conditions.” Dollar General has since been restructured and completed. The concern needs to be on the leverage multiples over 8x EBITDA. We profiled the First Data LBO, whose leverage was around 11x, in our last letter. Let me be very clear here: deals that are levered at greater than 6-7x and make it are the exception not the rule. It would seem that fundamentals are as bad as the technicals. The good news is that this is not 1998-2000 where we were levering up on no earnings (heck in most cases no revenues), so when the defaults start, it will be more “traditional”—bad balance sheet, decent business–leaving better recoveries. But then again, at 9-10x, maybe not. Where in the heck is that purple pill? Portfolio Strategy and Updates 4 source: “The Bloom’s Off the Liquidity Rose”- Jeffrey Rosenberg, July 2, 2007

Okay, so why is it that we’re sounding so happy about all this? Well, it’s always difficult to know what to cheer for, but problems create volatility and volatility creates opportunity. Our style is one of opportunistic lending. The last good bout of volatility was created in May of 2005 when Ford and GM were downgraded to junk ratings. Not coincidentally, we ramped and closed our second CBO during that month. Since then, spreads have been grinding tighter and prices higher in the loan and bond markets. A very large part of our market had taken the opportunity to refinance their higher cost paper and we have seen plenty of 8% coupons trading at or above par. In this market we have been challenged to find decent yields and even more challenged to find discounts on bonds we feel were not “value traps” (cheap but cheap for the right reasons, rather than undervalued bonds). We are finally starting to see the discounts showing up and new paper being issued with real (double digit) coupons. This is the beginning of a power shift from the issuers to the buyers. I fully expect that this weakness will continue and likely pick up speed over the next quarter. Our strategy is to deploy capital into the following situations:

Companies that have stable demand profiles and generate free cash flow.

Companies that have “market adjusted debt” or “MAD” ratios significantly below

In a perfect world, both will exist. Interestingly, we are now seeing the opportunity to do just this by selling some of our higher priced more cyclical names and acquiring what we feel are non-cyclicals at deeper discounts. Our goal is to clip the coupons while we wait for the discounts to be shrunk. Conclusion: Interestingly, my conclusion in our last letter spoke about the end of the golden era for issuers when and if buyers finally wake up. Well, buyers are now wide eyed and in no mood for “Covenant Lite” or “PIK Toggle” transactions. It has been about two years since we have seen the market sell off with such vigor and we plan on taking advantage of this opportunity to deploy cash in what we feel are excellent values. We look forward to updating you on these transactions next quarter. As always, feel free to call with any questions. Sincerely, PERITUS I ASSET MANAGEMENT, LLC Timothy J. Gramatovich, CFA Chief Investment Officer Peritus I Asset Management Return Disclosure: Although information and analysis contained herein has been obtained from sources Peritus I Asset Management, LLC believes to be reliable, its accuracy and completeness cannot be

guaranteed. This report is for informational purposes only. Any recommendation made in this report may not be suitable for all investors. As with all investments, investing in high yield corporate bonds and other fixed income securities involves various risks and uncertainties, as well as the potential for loss. Past performance is not an indication or guarantee of future results.

Interestingly, the world of bonds and loans appears to be suffering from some of these same digestive ailments. As my above question suggests, just how serious this market problem ultimately becomes is open to debate. However, it appears that nobody now denies that some medication is going to be required. This in itself is a drastic flip flop from no more than six weeks ago. As we profiled in our last letter, the credit markets had gotten downright silly. Buyouts were being done at leverage multiples that almost guaranteed a bankruptcy filing within a couple years of completing the transaction. Stupid acronyms began popping up. Among those were things like “PIK Toggle” and “Covenant-Lite.” As we discussed, these concepts and names get created at the top of cycles to allow acquirers to overpay for transactions. The table on the left represents the Covenant-Lite (the removal of covenants outlining certain minimum performance metrics that must be met) loan issuance as a percentage of total leveraged loan issuance. The table on the right shows what percentage the PIK Toggle represented as a percentage of total bond issuance1:

So by the looks of this, we have we eaten lots of real “junk food” in the first half of 2007. But there is another factor at play: it appears that our mouths have become substantially bigger than our stomachs. We know that the private equity coffers are loaded with equity money for deals, but a large portion of the total deal value (generally around 75%) is financed with debt not equity, so the high yield bond market and leveraged loan market have to be open for business or it’s no mas. This is where the problems begin. There was a basic assumption that with risk free rates and defaults both low, deals will be able to get financing. Unfortunately, this is a fallacy, as money is a relatively finite commodity. Investors allocate money to various asset classes and money managers invest it. We know that private equity has been well funded, but what about the high yield and loan buyers? Well, high yield has not had much money flow. Through this week, high yield mutual funds have experienced NO net money flows.2 Other big investors allocate sparingly to high yield bonds. High yield institutional searches have slowed to a crawl and high yield bond CBO’s haven’t been popular since they crashed and burned in the early part of this decade. However, one constant source of cash is the natural reinvestment process as

1 source: “The Bloom’s Off the Liquidity Rose”- Jeffrey Rosenberg, July 2, 2007 2 source: S&P LCD 7-12-07

Interestingly, the world of bonds and loans appears to be suffering from some of these same digestive ailments. As my above question suggests, just how serious this market problem ultimately becomes is open to debate. However, it appears that nobody now denies that some medication is going to be required. This in itself is a drastic flip flop from no more than six weeks ago. As we profiled in our last letter, the credit markets had gotten downright silly. Buyouts were being done at leverage multiples that almost guaranteed a bankruptcy filing within a couple years of completing the transaction. Stupid acronyms began popping up. Among those were things like “PIK Toggle” and “Covenant-Lite.” As we discussed, these concepts and names get created at the top of cycles to allow acquirers to overpay for transactions. The table on the left represents the Covenant-Lite (the removal of covenants outlining certain minimum performance metrics that must be met) loan issuance as a percentage of total leveraged loan issuance. The table on the right shows what percentage the PIK Toggle represented as a percentage of total bond issuance1:

So by the looks of this, we have we eaten lots of real “junk food” in the first half of 2007. But there is another factor at play: it appears that our mouths have become substantially bigger than our stomachs. We know that the private equity coffers are loaded with equity money for deals, but a large portion of the total deal value (generally around 75%) is financed with debt not equity, so the high yield bond market and leveraged loan market have to be open for business or it’s no mas. This is where the problems begin. There was a basic assumption that with risk free rates and defaults both low, deals will be able to get financing. Unfortunately, this is a fallacy, as money is a relatively finite commodity. Investors allocate money to various asset classes and money managers invest it. We know that private equity has been well funded, but what about the high yield and loan buyers? Well, high yield has not had much money flow. Through this week, high yield mutual funds have experienced NO net money flows.2 Other big investors allocate sparingly to high yield bonds. High yield institutional searches have slowed to a crawl and high yield bond CBO’s haven’t been popular since they crashed and burned in the early part of this decade. However, one constant source of cash is the natural reinvestment process as

1 source: “The Bloom’s Off the Liquidity Rose”- Jeffrey Rosenberg, July 2, 2007 2 source: S&P LCD 7-12-07

investors receive cash flows from their coupons and get principal back through the call or tender of their bonds. But this amount is not even close to closing the demand gap. Below we have profiled the deals expected to come to market shortly in just the bond area that exceed $1 billion. 3 These amounts are all in millions of dollars.

investors receive cash flows from their coupons and get principal back through the call or tender of their bonds. But this amount is not even close to closing the demand gap. Below we have profiled the deals expected to come to market shortly in just the bond area that exceed $1 billion. 3 These amounts are all in millions of dollars.

going to require a pretty stiff dose of Tagamet or maybe Prilosec. To determine if the Nexium is a better bet we should take a brief gander at the fundamentals of our world. A Fundamental Question Liquidity does funny things to perfectly rational people. It takes away healthy skepticism and caution and replaces it with hubris accompanied by boldness. We prefer to call it delusional. The chart below profiles historical leverage ratios next to some recently proposed transactions.4

Focus on the last four bars. I must confess that I do not know what parameters were used for “LBO Large Corporate,” but it appears to be understating the amount of leverage employed. The last three bars represent transactions that were pulled from the bond market because of “current conditions.” Dollar General has since been restructured and completed. The concern needs to be on the leverage multiples over 8x EBITDA. We profiled the First Data LBO, whose leverage was around 11x, in our last letter. Let me be very clear here: deals that are levered at greater than 6-7x and make it are the exception not the rule. It would seem that fundamentals are as bad as the technicals. The good news is that this is not 1998-2000 where we were levering up on no earnings (heck in most cases no revenues), so when the defaults start, it will be more “traditional”—bad balance sheet, decent business–leaving better recoveries. But then again, at 9-10x, maybe not. Where in the heck is that purple pill? Portfolio Strategy and Updates 4 source: “The Bloom’s Off the Liquidity Rose”- Jeffrey Rosenberg, July 2, 2007

Okay, so why is it that we’re sounding so happy about all this? Well, it’s always difficult to know what to cheer for, but problems create volatility and volatility creates opportunity. Our style is one of opportunistic lending. The last good bout of volatility was created in May of 2005 when Ford and GM were downgraded to junk ratings. Not coincidentally, we ramped and closed our second CBO during that month. Since then, spreads have been grinding tighter and prices higher in the loan and bond markets. A very large part of our market had taken the opportunity to refinance their higher cost paper and we have seen plenty of 8% coupons trading at or above par. In this market we have been challenged to find decent yields and even more challenged to find discounts on bonds we feel were not “value traps” (cheap but cheap for the right reasons, rather than undervalued bonds). We are finally starting to see the discounts showing up and new paper being issued with real (double digit) coupons. This is the beginning of a power shift from the issuers to the buyers. I fully expect that this weakness will continue and likely pick up speed over the next quarter. Our strategy is to deploy capital into the following situations:

Companies that have stable demand profiles and generate free cash flow.

Companies that have “market adjusted debt” or “MAD” ratios significantly below

going to require a pretty stiff dose of Tagamet or maybe Prilosec. To determine if the Nexium is a better bet we should take a brief gander at the fundamentals of our world. A Fundamental Question Liquidity does funny things to perfectly rational people. It takes away healthy skepticism and caution and replaces it with hubris accompanied by boldness. We prefer to call it delusional. The chart below profiles historical leverage ratios next to some recently proposed transactions.4

Focus on the last four bars. I must confess that I do not know what parameters were used for “LBO Large Corporate,” but it appears to be understating the amount of leverage employed. The last three bars represent transactions that were pulled from the bond market because of “current conditions.” Dollar General has since been restructured and completed. The concern needs to be on the leverage multiples over 8x EBITDA. We profiled the First Data LBO, whose leverage was around 11x, in our last letter. Let me be very clear here: deals that are levered at greater than 6-7x and make it are the exception not the rule. It would seem that fundamentals are as bad as the technicals. The good news is that this is not 1998-2000 where we were levering up on no earnings (heck in most cases no revenues), so when the defaults start, it will be more “traditional”—bad balance sheet, decent business–leaving better recoveries. But then again, at 9-10x, maybe not. Where in the heck is that purple pill? Portfolio Strategy and Updates 4 source: “The Bloom’s Off the Liquidity Rose”- Jeffrey Rosenberg, July 2, 2007

Okay, so why is it that we’re sounding so happy about all this? Well, it’s always difficult to know what to cheer for, but problems create volatility and volatility creates opportunity. Our style is one of opportunistic lending. The last good bout of volatility was created in May of 2005 when Ford and GM were downgraded to junk ratings. Not coincidentally, we ramped and closed our second CBO during that month. Since then, spreads have been grinding tighter and prices higher in the loan and bond markets. A very large part of our market had taken the opportunity to refinance their higher cost paper and we have seen plenty of 8% coupons trading at or above par. In this market we have been challenged to find decent yields and even more challenged to find discounts on bonds we feel were not “value traps” (cheap but cheap for the right reasons, rather than undervalued bonds). We are finally starting to see the discounts showing up and new paper being issued with real (double digit) coupons. This is the beginning of a power shift from the issuers to the buyers. I fully expect that this weakness will continue and likely pick up speed over the next quarter. Our strategy is to deploy capital into the following situations:

Companies that have stable demand profiles and generate free cash flow.

Companies that have “market adjusted debt” or “MAD” ratios significantly below